Why Nigeria Is Ready for Digital Cards — And How Safe Haven Is Leading the Change

The cashless revolution succeeded. Now, it's time for the next chapter.

If you travelled back to a Nigerian bank in the early 1990s, you’d find a world that feels lightyears away from today. It was the era of the "tally number", a physical metal tag you’d receive after hours of waiting in line just to prove your place. Banking was a stationary, exhausting task that required physical presence, manual ledger entries, and a lot of patience. If you needed to send money to someone in another state, you either braved the "night bus" or sent a relative with a bag of cash. We were a society tethered to paper and physical proximity, where the idea of "instant" anything was a fantasy.

Even though banking felt entirely physical at the time, the first quiet shift was already beginning. In the early 1990s, Nigerian banks started introducing ATM cards, simple tools that allowed customers to withdraw cash without entering the banking hall. These early cards were limited in function, but they marked the beginning of a shift away from purely manual banking and toward electronic access.

The turn of the millennium marked the beginning of a digital awakening, unfolding in three distinct stages that redefined our relationship with money. It started in the late 1990s and early 2000s with the birth of Internet Banking. For the first time, Nigerians could view balances and initiate transactions via desktop browsers. While revolutionary, it was still restrictive, requiring a bulky PC and a stable dial-up connection.

Then, between 2008 and 2012, the Mobile Banking App era arrived, driven by the global smartphone explosion. Banking moved from the desk to the pocket, allowing us to transact on the go. Interestingly, USSD banking followed between 2013 and 2016, specifically tailored for the Nigerian landscape. By using simple strings of code on feature phones, it bridged the gap for millions with limited internet access, ensuring that banking wasn't just for those with expensive smartphones.

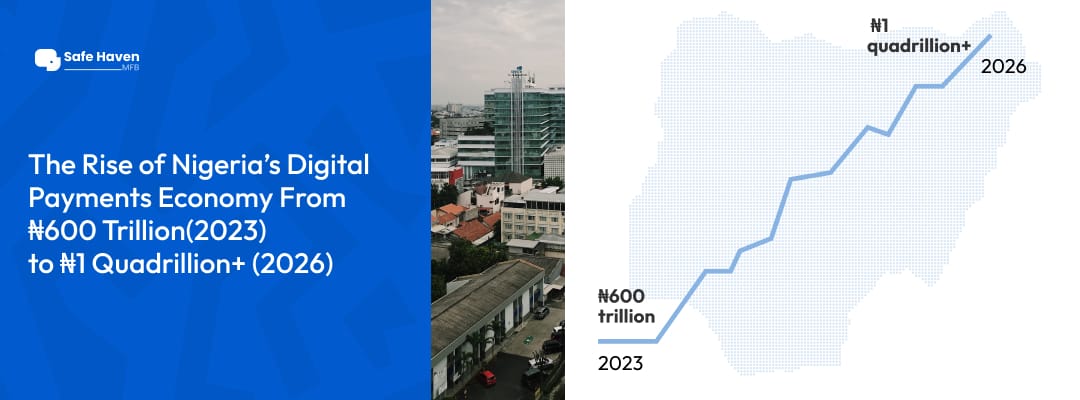

This technological foundation paved the way for an explosion in growth. By 2023, the transformation reached a fever pitch, with Nigeria recording over ₦600 trillion in electronic payment transactions. Today, in 2026, the data is even more impressive, with e-payments surpassing ₦1 quadrillion annually. We have evolved into a society that expects speed and reliability as a default. However, even with this progress, one relic of the past remains in our pockets, the plastic cards. It’s expensive to replace, easy to lose, and often takes days to deliver.

But as this digital ecosystem expanded, it also became clear that convenience comes with structure, and structure comes with cost. Behind this rapid transformation is a less discussed reality: digital banking is not truly “free.” Banks and financial institutions generate significant revenue from transaction fees, maintenance charges, interchange fees on card payments, and service charges across mobile and online platforms.

Even USSD banking, originally designed for inclusion, has evolved into a steady revenue stream. Following the Nigerian Communications Commission (NCC) End-User Billing framework, customers now pay per USSD session, with charges deducted from airtime, meaning every balance check or transfer carries a small cost. These accumulated micro-charges, when scaled across millions of users, contribute heavily to the earnings of banks, mobile network operators, and other players in the digital financial ecosystem.

This brings us to the final frontier of our payment evolution: the Safe Haven Digital Card. Built on the advanced Sudo infrastructure, Safe Haven is leading the charge by turning your smartphone into a high-tech payment hub. Unlike traditional virtual cards that only work for online shopping, this is Nigeria’s first fully functional digital card that mimics everything a physical & virtual card can do. Using NFC (Near Field Communication), you can simply tap-to-pay at a POS terminal or ATM. Safe Haven Digital Card is designed for the "now" generation, those who don't have the time to visit a bank branch or handle the long wait for a courier. With Safe Haven, you can get a digital card for as low as ₦100, effectively ending the cycle of paying high fees for damaged or lost plastic cards.

Digital banking only works when it fits local realities. That is why our Safe Haven Digital Card functions both online and offline. Even when mobile data finishes or network connectivity becomes unstable, transactions can still be completed. This flexibility is essential in many parts of Nigeria where internet service can be unreliable, yet daily transactions must continue without interruption.

In countries like the US, UK, China, and across Europe, contactless payments are already part of daily life. Platforms such as Apple Pay and Google Pay have turned smartphones into Digital cards, letting people pay for transport, groceries, and coffee with a simple tap. The COVID-19 pandemic accelerated this shift globally, as people became more conscious about avoiding physical contact and handling cash or cards unnecessarily.

Businesses and consumers quickly embraced “tap-to-pay” as a safer, faster, and more convenient way to transact. These services showed the world something important: once payments become fast and effortless, people rarely want to return to plastic cards or cash. Nigeria is now at that same turning point. Our habits are already digital, smartphone use is widespread, and the infrastructure is catching up. What was missing was a solution built for local realities and that’s where Safe Haven Digital Card comes in.

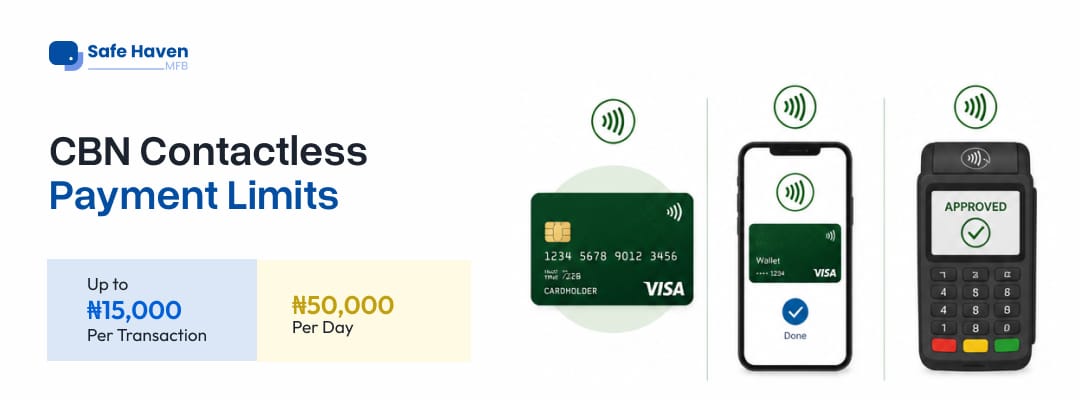

Actually, this move toward "tap-to-pay" isn't just a trend; it's a regulated evolution. The Central Bank of Nigeria (CBN) paved the way by releasing official Guidelines on Contactless Payments. Think of these guidelines as the final piece of the puzzle that makes Nigeria truly ready for digital cards. To keep us all safe, the CBN set a single transaction limit of ₦15,000 and a daily cumulative limit of ₦50,000 for contactless payments. This means you can breeze through a supermarket or a pharmacy by just tapping your phone, but if a transaction goes above those limits, the system kicks in with extra verification like a PIN or biometric check. It’s the perfect balance of "fast" and "secure."

What makes this transition so seamless is how Safe Haven accounts for the reality of the Nigerian market. While we have over 5.9 million active PoS terminals nationwide, not every POS or smartphone is "tap-to-pay" ready yet. Safe Haven bridges this gap by generating a dynamic QR code that merchants can scan, ensuring you are never stranded regardless of the hardware available.

We are ready for this change because our history proves we crave efficiency. We’ve evolved from paper passbooks to plastic cards, and now, we are ready to embrace a world where your wallet is as digital as your conversations. Don’t just read about the future of payments, be part of it. Discover how the Safe Haven Digital Card can change the way you pay, spend, and move through your day.

Safe Haven isn't just offering a new product, it’s providing the logical conclusion to a journey that started in those long bank queues decades ago.